The Exchange as the Trade: Why Singapore Exchange Shares Sit at a Record

Shares of the Singapore Exchange reached a record in June, up more than half over the year. The operator does not rise on any single listing. It rises on turnover, because turnover is what its fees are charged on. And turnover across its markets has stepped up on a set of flows that look mostly structural rather than one-off.

Turnover is the fee base

The operator earns on volume. Securities daily average value is the single figure that most closely tracks its trading and clearing revenue, and its share price. That value rose about 62 percent from a year earlier in March, on record retail participation alongside rising institutional activity. Across the financial year to mid-2025, securities turnover had already grown about 28 percent to 336.4 billion Singapore dollars. More volume across the tape converts fairly directly into fee income, which is why the share moves with turnover rather than with any one deal. Turnover velocity, the share of market value that changes hands, has risen alongside the absolute figures, so the lift reflects more active trading of the existing base as well as new money arriving. That distinction matters, since velocity-led gains can persist as long as participation stays elevated.

The flows behind the volume

Several of the flows lifting turnover look structural. Safe-haven demand for the Singapore dollar has drawn money into the market. A domestic equity-market development programme has been deploying funds into small- and mid-cap names, broadening participation beyond the benchmark. Exchange-traded-fund turnover and assets reached records, with assets crossing a new threshold. Demand for the exchange's China-access futures has been strong, and open interest in its main China-index future reached a single-day record. Each of these adds to daily value without depending on a single listing. Exchange-traded-fund assets under management crossed a new high as gold and local fixed-income products drew inflows, and depository receipts that give access to regional underlyings added another turnover stream. The China-index future is the clearest single example: open interest reached a single-day record measured in the tens of billions of dollars of notional, a sign that offshore demand for China exposure is routing through the venue.

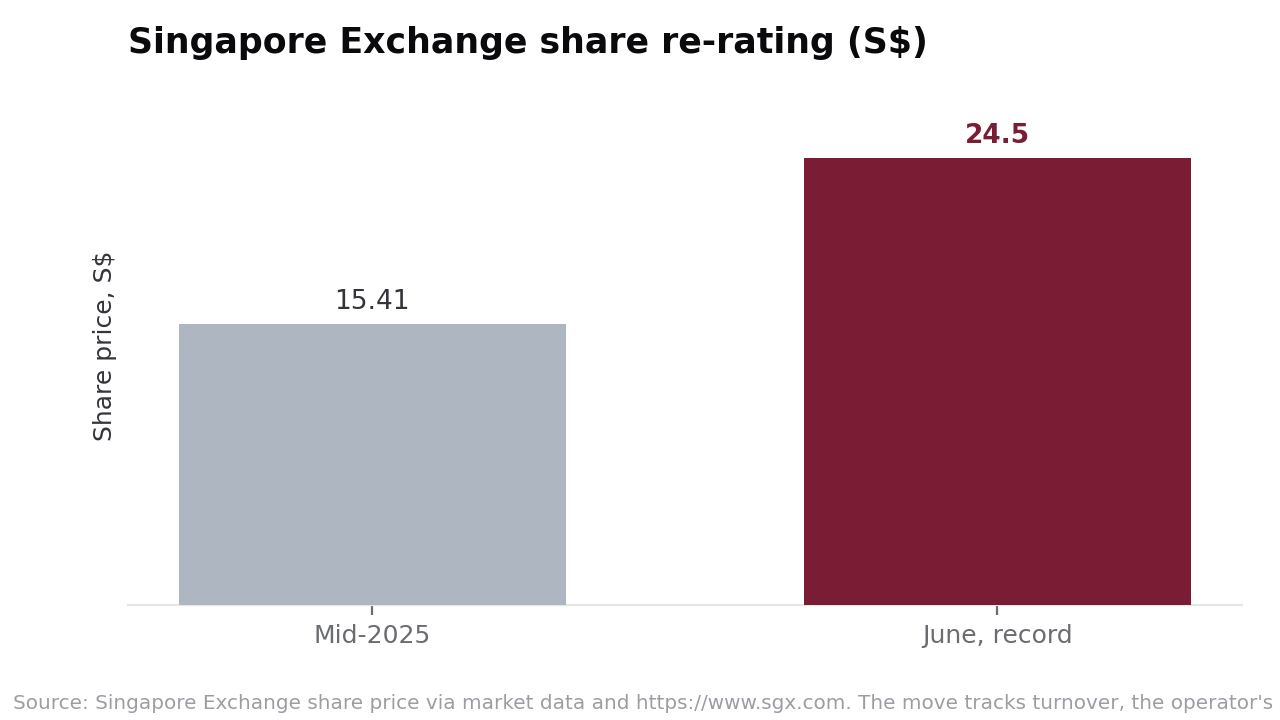

A re-rating on the driver

The share re-rated with that driver. It moved from about 15.41 Singapore dollars in the middle of last year to a record near 24.50 in June, a gain of more than 50 percent over twelve months, and a level last reached in 2007. The listing count did not drive it, having drifted lower over the same period. What changed was the amount of trading passing through the operator's books, and the fee income that follows from it.

What it rests on

The flows that lift turnover are the same ones that can fade. If safe-haven demand for the Singapore dollar eases, or the development-programme deployment slows, daily average value softens and the fee base with it. The exchange's own coverage frames much of the current demand as structural, tied to shifting reserve preferences and passive-product growth, rather than to a single event. One reading frames the shift in reserve preferences and the move into passive products as durable rather than cyclical, which would keep daily value elevated; another treats a share of the volume as tied to the current bout of market uncertainty, which would fade as it settles. The gauges to watch are the monthly daily-average-value print, the exchange-traded-fund and China-futures volumes, and the pace of the development-programme flows, for whether the record holds.