The Market the Rally Skipped: What Kept Hong Kong Stocks Behind

As global equities ran higher for most of the year, one major market trailed. Japanese, Korean, US technology and mainland Chinese tech-board benchmarks all advanced, while Hong Kong lagged and at times fell. By late June the Hang Seng Index sat near 22,672 after its worst week in over a year. Two mechanisms explain the gap: what the city's indices are made of, and where the money went.

A rally that skipped one market

The year's equity advance was broad. Benchmarks in Japan, Korea and the United States technology complex climbed, and the mainland's own tech boards ran hard. Hong Kong trailed the group and spent stretches of the year lower. The pattern turned sharper late in June, when the Hang Seng Index closed near 22,672 after its steepest weekly drop in more than a year, and the tech gauge slipped below levels it had held for months. That final leg down was not confined to Hong Kong: the mainland's STAR and ChiNext gauges, along with Korean and Taiwanese benchmarks, all fell in the same week as the Federal Reserve turned more hawkish and investors pressed for evidence that heavy artificial-intelligence spending would pay off. The lag, though, had been building well before that week.

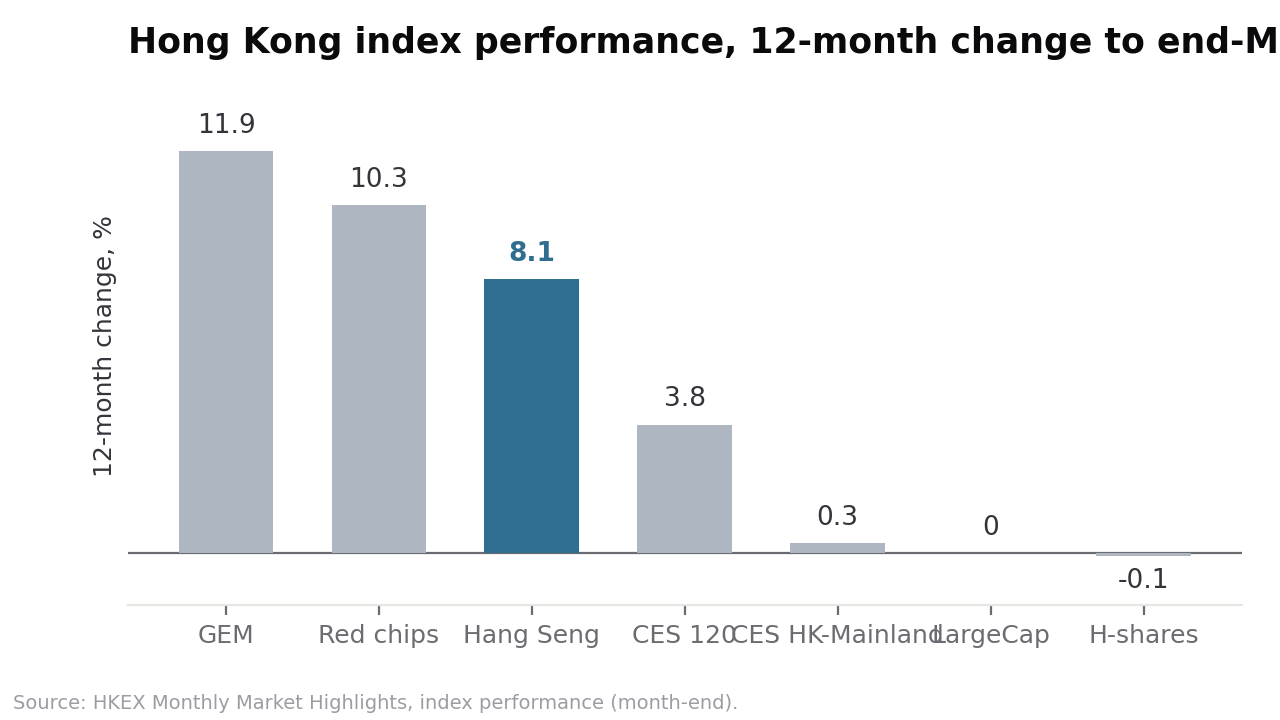

The split showed up across the exchange's own index performance. Over the year to end-May, the headline Hang Seng Index held an 8.1 percent gain and the red-chip and small-cap gauges led, while the China Enterprises index of mainland H-shares sat flat at minus 0.1 percent and the large-cap gauge at zero. Every one of those gauges then fell over the month of May, before June's drop pulled the market lower still.

What the indices are made of

The first mechanism is composition. Hong Kong's technology gauge is led by internet and consumer platforms, names such as Tencent, Alibaba, Meituan and Xiaomi, with limited exposure to the pure-play chip and artificial-intelligence hardware that lifted the US, Korean and Japanese benchmarks. So the index missed the leg of the global rally that ran through semiconductors and data-centre buildout. The platform companies also face their own squeeze. Core revenue in advertising, e-commerce and games has slowed as consumption stayed soft. Operating costs have risen where subsidy competition in areas like food delivery persisted longer than the market expected. And the platforms are spending heavily on artificial intelligence whose near-term return is unproven, so that spending reads for now as a drag on profit. One large platform reported revenue that missed expectations and fell sharply on the day, and a change to the mainland's electric-vehicle purchase tax added pressure to the auto names in the index.

Where the money went

The second piece is where the enthusiasm landed. The artificial-intelligence interest that the incumbent-heavy index missed showed up in new listings instead. Recently floated mainland model and AI names surged from their offer prices in early trading, with one large-model company up 523 percent, another up 488 percent, and a third AI group up 469 percent. Two of the large-model names were admitted to the tech index only in a May quarterly review. For much of the year, in other words, the capital chasing the AI theme in Hong Kong flowed into fresh IPOs, while the gauge that carries the technology label still held the older platforms. The result was a widening gap between the label and the leadership.

The flow seesaw

Flows did the rest. Hong Kong is an offshore market, so it is sensitive to global liquidity, and a more hawkish Federal Reserve pressed hardest on long-duration technology. At the same time, strength in the mainland's own tech boards pulled southbound money back north, a Hong Kong to mainland seesaw that a heavier calendar of Hong Kong IPOs and secondary offerings made worse by absorbing secondary-market cash. Brokerage research noted that southbound net inflows slowed through the year, having been a major support in the prior one. With foreign money already lighter than in past cycles, the swing in mainland flows carried more weight than usual.

What to watch

The gauges from here are the pace of southbound flows relative to the pull of the mainland boards, the internet platforms' core-revenue and AI-spending path, and the tech index's own composition as more artificial-intelligence names qualify for inclusion. Some analysts point to Hong Kong valuations sitting below their longer-run average as the reason they expect the discount to close, a case that rests on earnings expectations turning rather than on any single catalyst. Read against the year's global rally, the market's lag traces less to any one shock than to a structure and a flow backdrop that pointed the other way.