One label, two equity markets: Japan and Korea on the same wave

Two markets at records under the same AI banner. Underneath, they run on different fuel, and the gap between them is where a single-bucket read breaks.

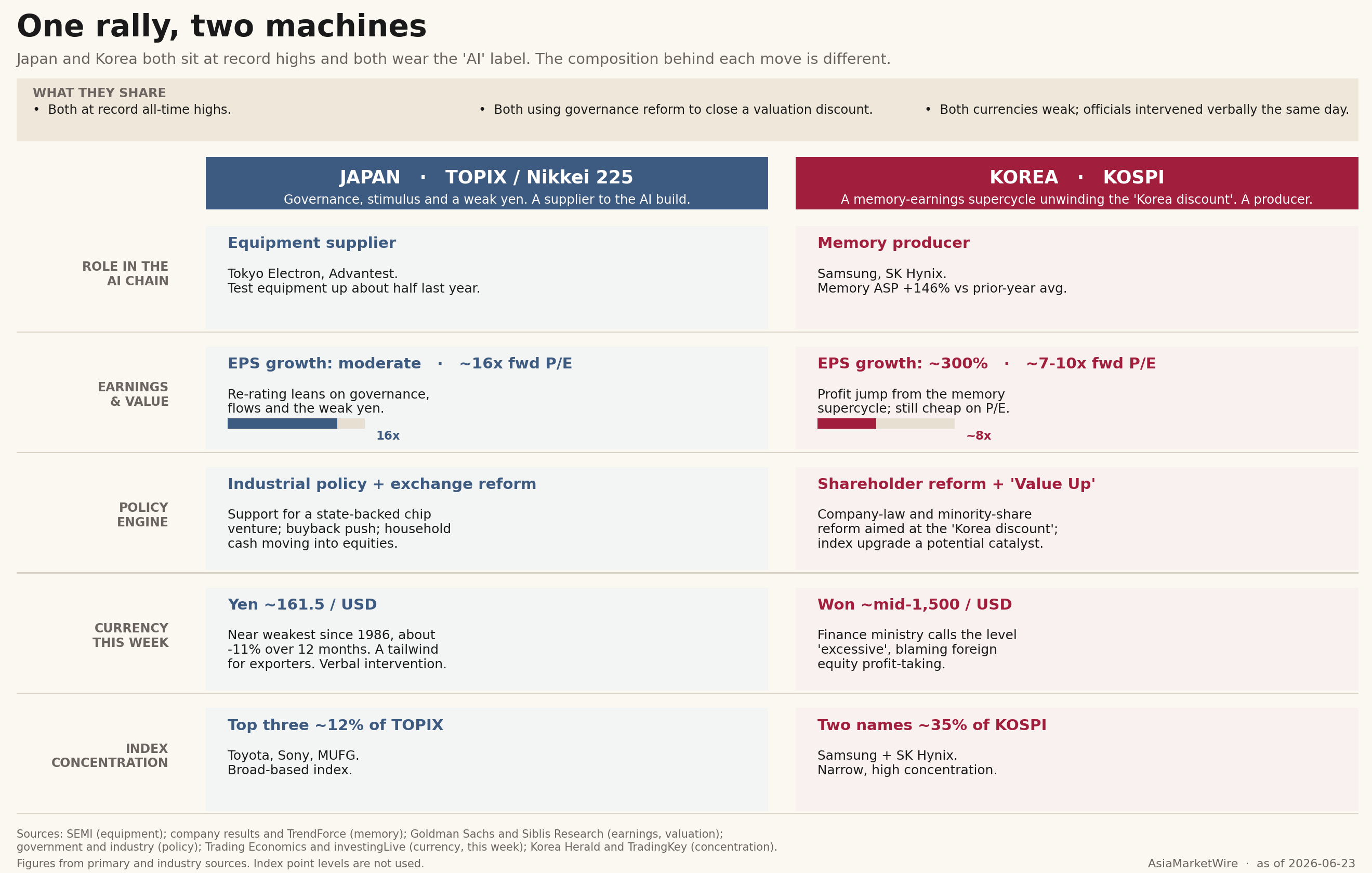

One trade, from a distance

Two of Asia's biggest equity markets sit at all-time highs, and from a distance they look like one trade. Both carry the same headline, the build-out of AI infrastructure. Both have a weak home currency their finance ministries keep trying to talk higher. Both are years into a governance program built to close a valuation gap that foreign money long treated as permanent. An allocator scanning the region can be forgiven for dropping them in one bucket: long Asia, long the chip cycle, hedge the currency, wait for the discount to close. That bucket is where the work goes wrong. The surface that invites a single trade sits on two markets running on different fuel, with different parts of the return doing the lifting and different things happening to the currency. Read as one position, they price one risk where there are two.

The read that travels

The version that moves fastest is the simplest: Japan and Korea are the non-US, non-China ways to own the AI cycle. It fits in a sentence, and a sentence is what crosses borders and lands in a committee deck. The compression is efficient, and it is also where the signal goes. What the sentence drops is the part that decides how each market moves once the wave shifts: where each country sits in the chain, which piece of the return is actually moving, and what the currency is doing and why. The gap here is about understanding, not information. The numbers are public and identical on every terminal. What separates a useful view from a crowded one is the willingness to pull the two markets apart and look at what each is made of. A single Asia AI basket is easy to build, easy to sell, and it rises when the chip names rise. A view that holds the two apart asks more of the reader and hands back no cleaner product. The information is commoditised. The reading is not.

Japan: a re-rating, with a supplier's seat

Japan's run is a re-rating before it is an earnings story. Its loudest AI exposure sits on the supply side. The country's champions sell the tools that make advanced chips, the deposition, etch and test machines every foundry and memory maker has to buy, rather than the chips themselves. Global chip-equipment billings hit a record near 135 billion dollars, up about 15 percent on SEMI's count, and the test-equipment slice one Japanese firm dominates rose by roughly half. A supplier rides the cycle one step back from the demand, banking the spending wave without the single-product risk of the firms doing the spending. Around that core sits the rest of the Japanese engine, and most of it has little to do with silicon. A decade-long push from the exchange has pressed companies into buybacks, fuller payouts and tighter use of capital, so the market's response is a multiple story before a profit one. Households that sat in cash for a generation have begun moving savings into stocks, a slow rotation of domestic money that gives the market a buyer with no currency view to spook it. The index is broad: its three biggest members make up only about an eighth of it, so no single stock runs the tape. The currency is the fourth leg, and the one most often misread. The yen sits near its weakest since 1986 for a market full of exporters, which is a tailwind, lifting earnings as they convert back into a cheaper home currency. Tokyo wants a floor under the yen while keeping the export edge the weakness brings. The softness is structural, rooted in the rate gap with the United States, and the central bank's slow normalisation has barely dented it. Japan's return comes from the multiple, the flows and the currency, with a supplier's claim on AI underneath. Profits are growing, at an ordinary pace.

Korea: an earnings shock, off a cheap base

Korea is the mirror image. Its rally is an earnings shock before anything else. The two memory makers that dominate the index sit on the production side of the same wave, and memory is where the AI build turns into raw operating leverage. As high-bandwidth memory crowds out commodity output and supply stays tight, contract prices have jumped hard. One large producer reported an average selling price for memory up about 146 percent against the prior year's average. Memory carries heavy fixed costs, so a price move that size drops to the bottom line with little to slow it down. One estimate put annual profit growth for the Korean benchmark near 300 percent, the strongest annual jump in Asia since the rebound from the regional crisis of the late 1990s. Where Tokyo re-rates, Seoul earns, and it earns off a low base. Even after the index roughly doubled, it trades at a multiple foreign money still reads as cheap. A value-up program paired with company-law changes that give minority owners more weight hands that cheapness a way to close, and a possible upgrade in global index classification dangles more passive money. The cost is concentration: two names carry about a third of the market's value, which makes the index a geared bet on one cycle and two balance sheets. The breadth that steadies Japan is exactly what Korea does without. The currency gives the structure away. The won sits near the weak end of its range, and Seoul has called the level excessive, blaming foreign equity profit-taking. In Japan the weak currency feeds the rally. In Korea the weak currency is partly the rally's own exhaust, as foreign money that bought the stocks rotates out of the won. The same inflows that lift the index push down on the currency, so strength in one shows up as weakness in the other. A loop like that runs both ways: if the money turns, selling in the stocks and pressure on the won feed each other on the way down.

Two logics on one wave

Put them side by side and the split is clean. Japan sits on the supply side of the chain, Korea on the production side. Japan's return is led by the multiple, the flows and a tailwind currency; Korea's by earnings off a cheap base. Japan's index is broad and its profit growth ordinary; Korea's is narrow and its profit growth historic. Japan's weak currency is an input to the rally; Korea's is a by-product of it. Both wear the AI label, and both have earned it, yet they claim it from opposite ends of the same chain and get paid in different coin. The shared items up top, the records, the soft currencies, the reform programs, the AI banner, are real. They are also the parts that compress most easily and travel furthest, which is why they end up standing in for the whole thing. The parts that resist compression, the seat in the chain and the driver of the return, are the parts that decide what each market does next.

Where the one trade breaks

Markets that went up for different reasons come down for different reasons. Korea's fault line is the memory cycle and its own concentration: the leverage that produced a triple-digit profit year runs the other way when prices roll over, and the currency-and-equity loop can tighten if foreign money steps back. Japan's fault line is elsewhere: a currency tailwind that flips to a headwind as the central bank tightens, or a flows-and-multiple advance that stalls with no single cycle to snap it. The drawdowns, when they come, will not land on the same day or run the same depth. An allocator holding Asia AI as one line runs one risk model for two risk profiles. The hedge that protects the currency leg in Tokyo does the wrong job in Seoul, where a weak won and strong stocks have moved together. A basket that looks diversified because it covers two countries is, on the cycle that actually matters, two takes on the same chip demand pointing in opposite directions. None of this picks one market over the other. The point is smaller and sturdier: they are different instruments, and an investor who prices them as one is carrying a risk they never measured. The headline squeezes the two into a sentence. What they are made of pulls them back apart. Same wave, two machines. Where a reader stands on which runs further is theirs to judge; the distinction is the part worth carrying.