From lever to toll: what the Hormuz trade is actually pricing

Markets price a chokepoint as a binary switch. The logic behind that framing, and the question of who pays for it, carries further than any day's barrel.

The barrel prices access, not supply

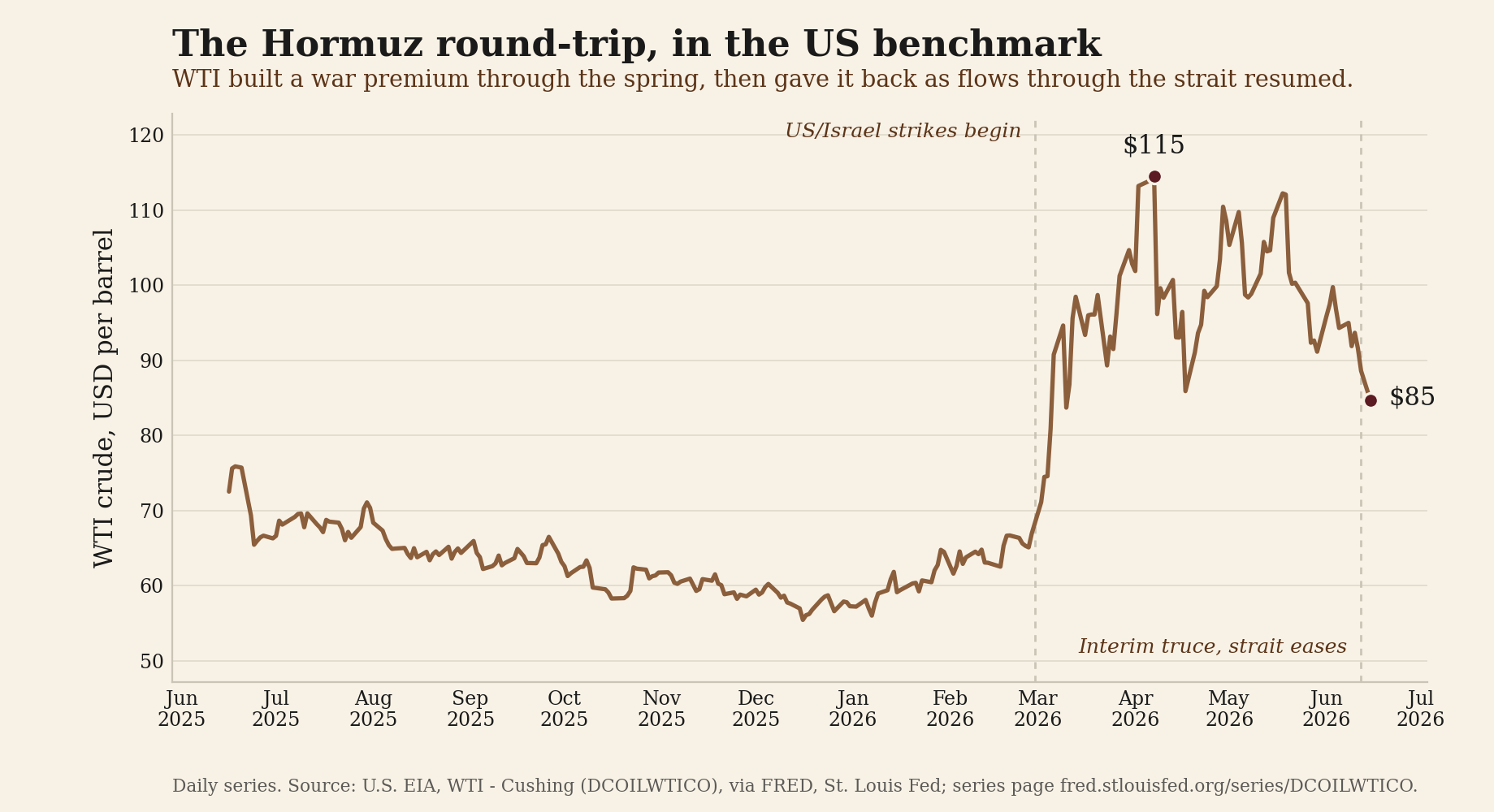

Through the spring of 2026 the oil market read one negotiation through a single question: is the Strait of Hormuz open or shut. A war premium went onto the price of crude as strikes on Iran raised the odds of closure, and it came off again as an interim understanding let traffic through the strait resume. That round trip is the tell. The barrel was pricing access to a passage. Reserves and production schedules sat to one side. Around a fifth of the world's seaborne crude moves through Hormuz, and because oil is fungible and clears at one global margin, the state of that single waterway can set the price of barrels that go nowhere near it. The premium is closer to insurance on a chokepoint than to an ordinary supply-and-demand story, loosely tied to the flow it stands in for. Read it as supply and demand and the mechanism is lost, which is the market quoting the odds on a gate.

From lever to toll

The more durable question is what happens to that gate over time. Tehran moved to turn it from a lever into a fee. It floated mandatory insurance on ships transiting the strait, free at first and billable later, and drafted legislation to charge for passage. The strait authority later added that vessels using routes outside its designated framework would forfeit any guarantee of safe passage, with the cost placed on owner and operator. The change in kind matters more than the numbers. An open-or-shut event, waited out once, becomes a standing claim on each cargo that crosses. A spike can be waited out. A toll is priced for as long as the lever exists, and it reaches cargo through war-risk insurance, the channel that turns a headline into a line on a freight bill.

The switch splits in two

The single switch did not hold as one variable. It divided into two that can point in opposite directions at once. One is political, the status of any ceasefire, which can crack on a single drone. The other is physical, the count of tankers actually crossing, which moves on storage, on loadings, and on whether owners judge the passage worth the risk. For a stretch the two ran together, so one number stood in for both. Then they diverged, and the price tracked the physical one. Crude settled toward a pre-war low even as a ceasefire understanding frayed, because the count of hulls kept climbing back toward pre-war levels while the political switch flipped the other way. The barrel priced the tankers above the truce. Behind both sits a third and slower variable, the nuclear file, measured in enrichment stocks and inspection access, moving on a clock of its own.

Where the cost lands

The sharper lens is incidence: who actually pays for a contested strait. Two seats sit at the table, Washington and Tehran. The cost lands downstream, on the importers who buy what flows through, and that demand sits mostly in Asia. It arrives through the currencies of energy importers and through the share prices of the refiners, shippers, and manufacturers that run on imported feedstock. China, a principal buyer of Gulf crude, carries the exposure while holding no chair in the room. The events made the geography literal. A struck vessel flew a Singapore flag. A paused evacuation covered ships along an Asia-facing route. War-risk insurance prices off exactly these incidents, which is the mechanism by which a strait that few local buyers control still sets what they pay.

No exemption at the margin

The same logic explains why a strait that almost no American barrel crosses still reaches an American pump. Pumping domestic oil buys no exemption once the price clears at the global margin. Refiners pay the world price, the domestic benchmark follows the international one through arbitrage, and because crude trades in dollars the cost arrives with no currency cushion to soften it. When energy supplied the bulk of a fresh pickup in headline inflation, a central bank that holds rates while marking a supply shock it cannot offset is reading the same gate the oil curve is reading, from the other end of it.

What the gauges are

Position around the framing rather than the headline price, and the instruments follow. The daily transit count reads whether the physical switch stays open. The insurance-and-fee proposals and the strait authority's framework rules read whether a lever is hardening into a charge. The nuclear track reads whether the decoupling that steadied the oil curve survives the harder file. Around the edges the cartel is under its own strain, with one member departed and another pressing for a larger quota. The barrel moves first. What it votes on is whether the hulls keep crossing, and who is allowed to send them. The vote is observable every day in the tanker count. Who is asked to honour it is the question the price does not print.